The Claude Effect

What Anthropic's latest models actually do, why markets are panicking, and how to position.

The Claude Effect Is Already Hitting Your Portfolio

On February 5, Anthropic dropped Claude Opus 4.6. Within days, software stocks were flashing red. By February 20, when the company unveiled Claude Code Security, the damage had spread deep into cybersecurity. A new AI automation tool from Anthropic sparked a $285 billion rout in stocks across the software, financial services, and asset management sectors in a single trading session. Then it got worse. CrowdStrike shares plunged 18% following the Claude Code Security launch, wiping out $20 billion in market capitalization. IBM recorded its biggest daily drop since 2000 at -13.2%.

Welcome to the Claude Effect.

This wasn’t a macro event. There was no Fed surprise, no recession signal, no earnings miss. What spooked markets was something harder to price: the dawning realization that AI is no longer supplementing software workflows — it’s replacing them. And the company at the center of it all just raised the stakes considerably.

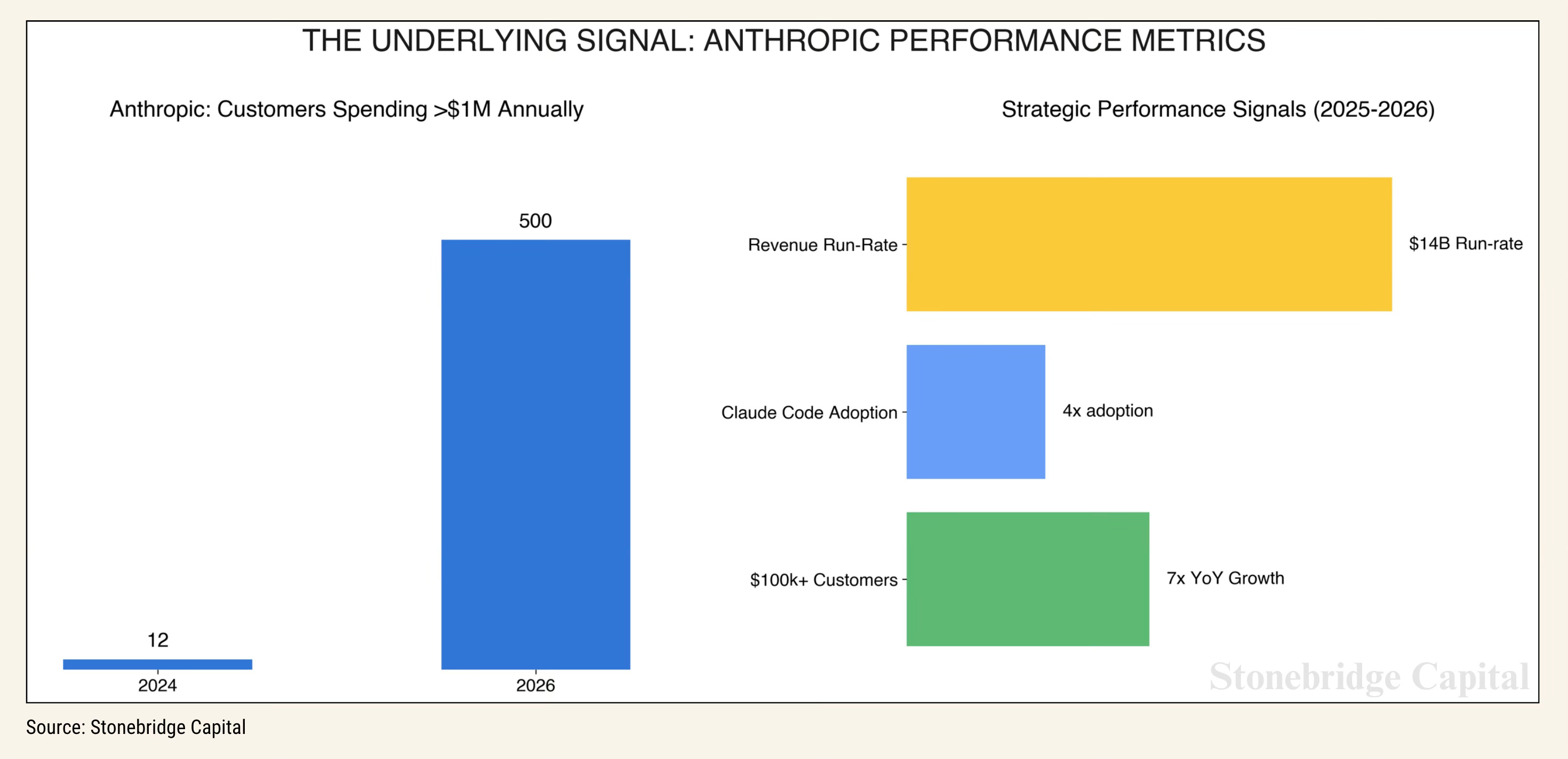

On February 12, Anthropic closed a $30 billion Series G funding round led by GIC and Coatue, valuing the company at $380 billion post-money. The company’s run-rate revenue now stands at $14 billion, growing more than 10x annually for each of the past three years. Eight of the Fortune 10 are now Claude customers. Claude Code alone has crossed $2.5 billion in annualized revenue — more than double its level at the start of the year.

The financing marks the largest venture deal of 2026 so far and the second-largest of all time, following only OpenAI’s $40 billion round in 2025.

The picture that emerges is one of a company generating real enterprise revenue, accelerating product launches at a pace that rivals aren’t matching, and disrupting entire industry categories with each release. For investors, that’s both an opportunity and an alarm bell — depending which side of the disruption you’re on.

Opus 4.6 and Sonnet 4.6, Broken Down

The Agentic Flagship

The headline feature is “agent teams.” Instead of one agent working through tasks sequentially, teams of agents can split larger tasks into segmented jobs, with each owning its piece and coordinating directly with the others. Anthropic’s head of product described this as having a talented team working in parallel, rather than a single contractor going through a checklist.

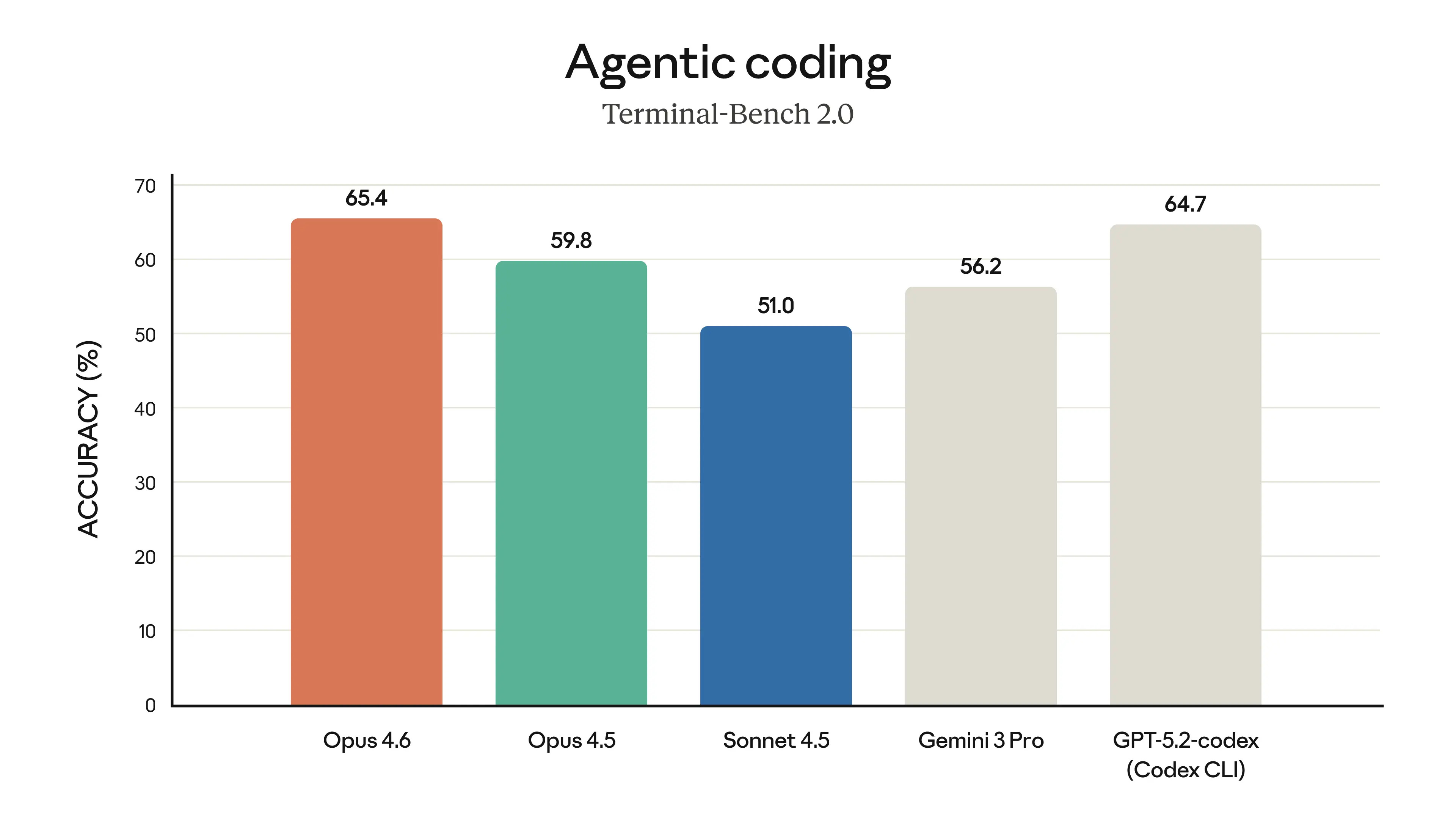

The most dramatic benchmark jump was on ARC AGI 2, where Opus 4.6 scored 68.8% compared to Opus 4.5’s 37.6%, an 83% improvement. On BrowseComp, its agentic web search benchmark, the model scored 84.0% versus Opus 4.5’s 67.8%.

Opus 4.6 supports a 200K context window, with a 1M token context window available in beta. It also supports adaptive thinking — Claude dynamically decides when and how much to think — along with 128K max output tokens and extended thinking.

Opus 4.6 also integrates Claude directly into PowerPoint as an accessible side panel. Previously, a user could tell Claude to create a PowerPoint deck, but the file would then have to be transferred to PowerPoint to edit. Now the presentation can be crafted within PowerPoint, with direct help from Claude.

Claude Opus 4.6 has already identified over 500 vulnerabilities across various open-source codebases during internal stress testing — bugs that had slipped through the cracks for decades despite multiple rounds of expert review.

As of February 20, it is the model with the longest task-completion time horizon as estimated by METR, with a 50% time horizon of 14 hours and 30 minutes. That number matters for agentic workflows. Legacy enterprise software doesn’t think. Claude does — for half a working day, autonomously.

The Value Bomb

If Opus 4.6 is the power player, Sonnet 4.6 is the one that should be keeping SaaS executives up at night. Performance that would have previously required reaching for an Opus-class model — including on real-world, economically valuable office tasks — is now available with Sonnet 4.6.

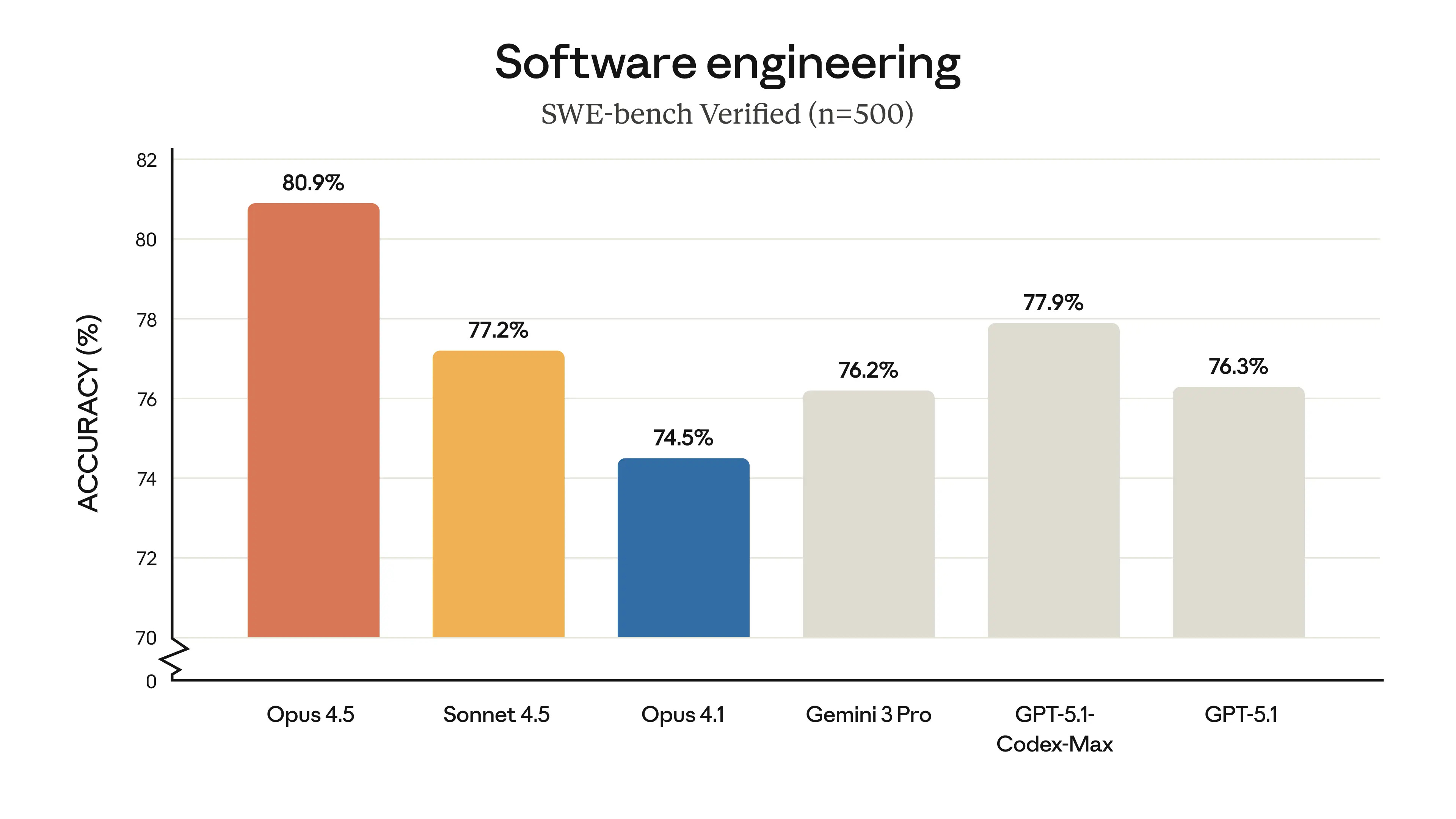

The new Claude Sonnet is priced at $3/$15 per million input/output tokens, compared to $5/$25 for Opus. It delivers near-flagship performance across most tasks while outperforming Opus 4.6 on office productivity (1633 vs 1559 Elo) and financial analysis (63.3% vs 62.0%).

In Claude Code, early testing found that users preferred Sonnet 4.6 over Sonnet 4.5 roughly 70% of the time. Users even preferred Sonnet 4.6 to Opus 4.5 — Anthropic’s frontier model from November — 59% of the time. They rated it as significantly less prone to overengineering and “laziness,” and meaningfully better at instruction following, with fewer false claims of success and fewer hallucinations.

Sonnet 4.6 became the default model for Free and Pro plan users on launch day. The beta release includes a context window of 1 million tokens, twice the size of the largest window previously available for Sonnet — enough to hold entire codebases, lengthy contracts, or dozens of research papers in a single request.

The cost math here is important. You’re getting near-flagship intelligence at 40% of flagship pricing, now available to every free claude.ai user by default. That’s not incremental progress. That’s democratization.

The Stock Whisperer Capabilities

This is where the disruption thesis gets concrete for finance professionals. Opus 4.6 now leads the Finance Agent v1.1 benchmark outright, which evaluates how well agents perform on core financial analyst tasks including research, financial analysis, and running analyses. Sonnet 4.6 actually edges it out slightly on that specific benchmark at 63.3%.

What does this mean in practice? A single Claude session can now:

Pull and analyze 10-K and SEC filings autonomously, build multi-scenario DCF models with Monte Carlo simulations, draft investment memos, run sentiment analysis on earnings transcripts across 10 dimensions, screen equities against custom criteria, and produce actionable research — all without leaving the chat interface.

Claude Sonnet 4.6 matches Opus 4.6 performance on OfficeQA, which measures how well a model can read enterprise documents (charts, PDFs, tables), pull the right facts, and reason from those facts. It’s a meaningful upgrade for document comprehension workloads.

A few prompts worth testing yourself:

“Act as a senior equity analyst. Pull the latest 10-K for [ticker], build a 5-year DCF with base, bull, and bear cases, identify the top three risk factors, and format the output as an investment memo.”

“Review this earnings call transcript and the last two quarterly filings. Score sentiment on 10 dimensions: revenue quality, margin trajectory, management confidence, competitive positioning, guidance credibility, and so on. Then suggest two trade ideas with entry levels.”

These aren’t hypotheticals — they work today, they’re accessible on the free tier for simpler tasks and on Pro and Max plans for the full agentic stack.

The broader implication: junior analyst work, FactSet data queries, due diligence checklist items — all of these are now tasks Claude can complete faster and cheaper than a human doing them manually. That’s the alpha opportunity for early adopters, and the disruption threat to data vendors selling access to what Claude can now synthesize itself.

Why Software Stocks Are Bleeding

This wasn’t a single catalyst. It’s been a rolling series of shocks across January and February 2026, each one hitting a different corner of the software market.

The Cowork Shock (Late January / Early February)

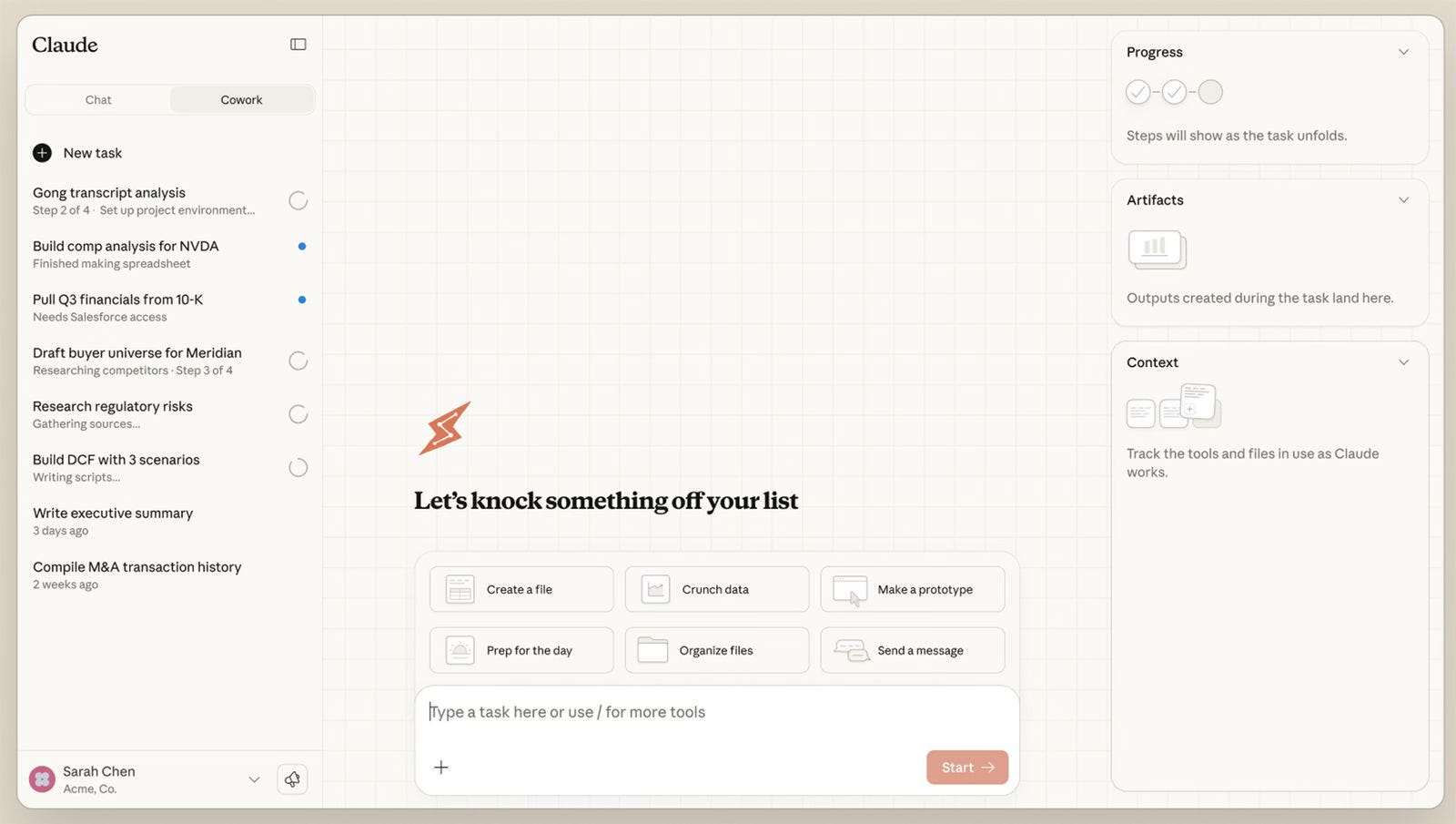

The selloff began with Claude Cowork. Claude Cowork is designed to act like an AI colleague, with the ability to read files, organize folders, and draft documents. New plugins tailored for specific industries — sales, finance, data marketing, and legal — launched in late January. The plugins were released under an open-source license, enabling customization.

Thomson Reuters, operator of the legal database Westlaw, recorded a price decline of almost 18 percent. British competitor RELX (LexisNexis) lost 14.4% in a single day. Dutch provider Wolters Kluwer lost around 13%. Analysts attributed the losses to the fact that Anthropic’s legal plugin can take over functions such as reviewing confidentiality agreements, compliance checks, and the creation of legal briefings.

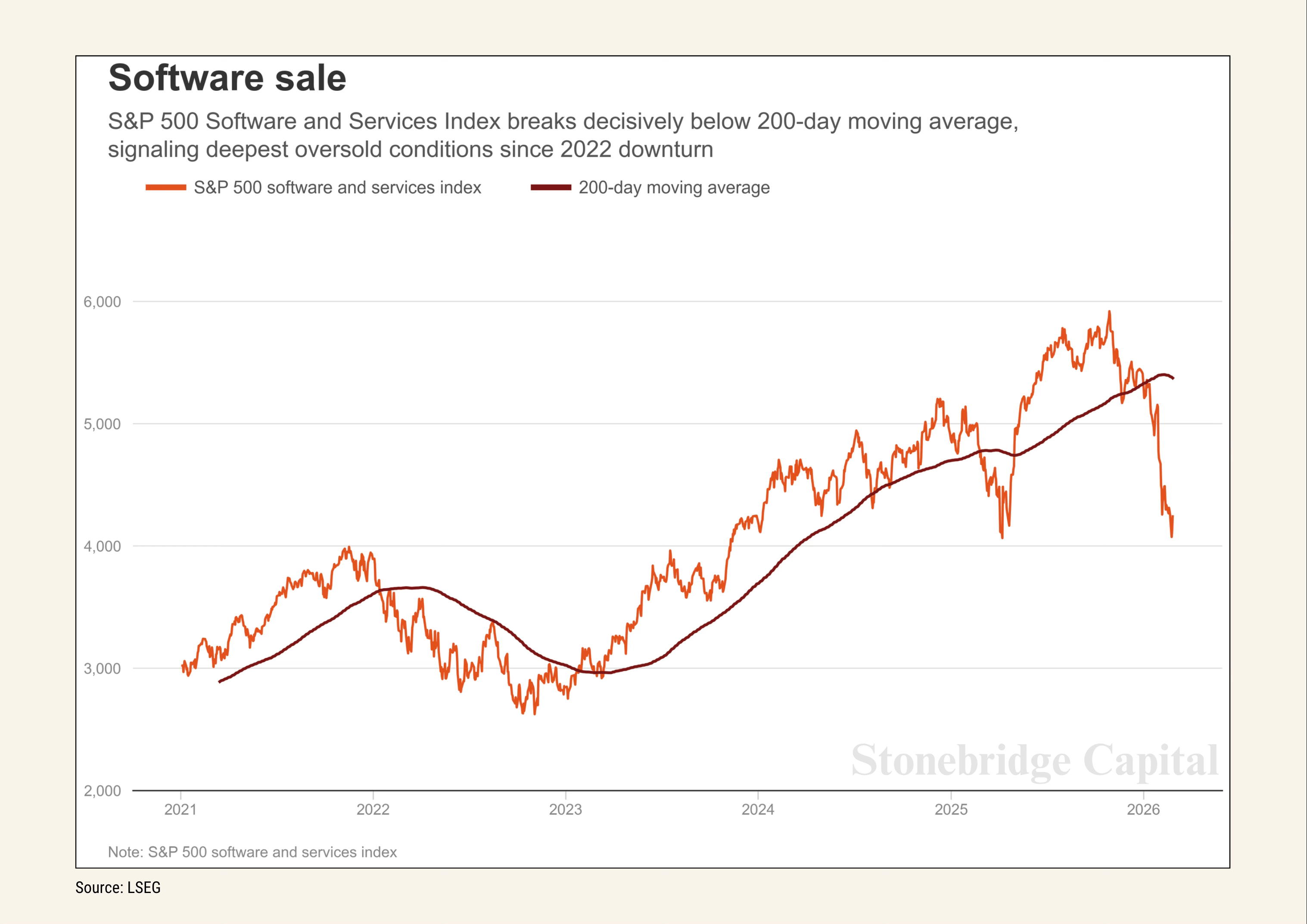

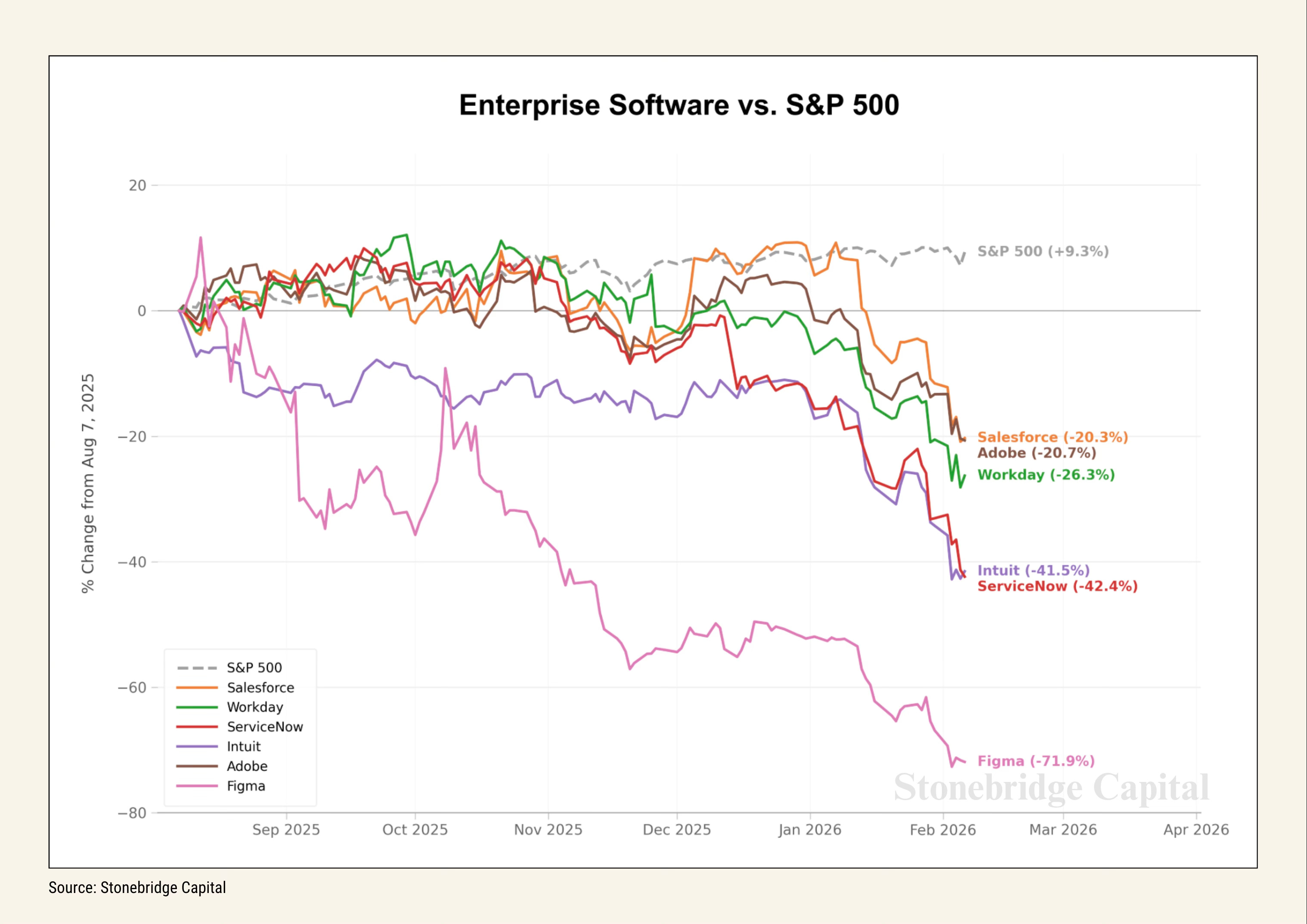

The iShares Expanded Tech-Software Sector ETF (IGV) is down over 23% year-to-date in 2026. Salesforce and Workday are each down over 40% in the past 12 months. Software price-to-sales ratios have compressed from 9x to 6x, levels not seen since the mid-2010s.

The S&P 500 Software & Services Index, which has 140 constituents, fell over 4% in a single session, extending its losing streak to eight sessions. The index is down about 20% so far this year. Shares of Thomson Reuters, Salesforce, and LegalZoom were among the hardest hit, with the selloff spreading to Asian IT firms Tata Consultancy Services and Infosys.

The Cybersecurity Flash Crash

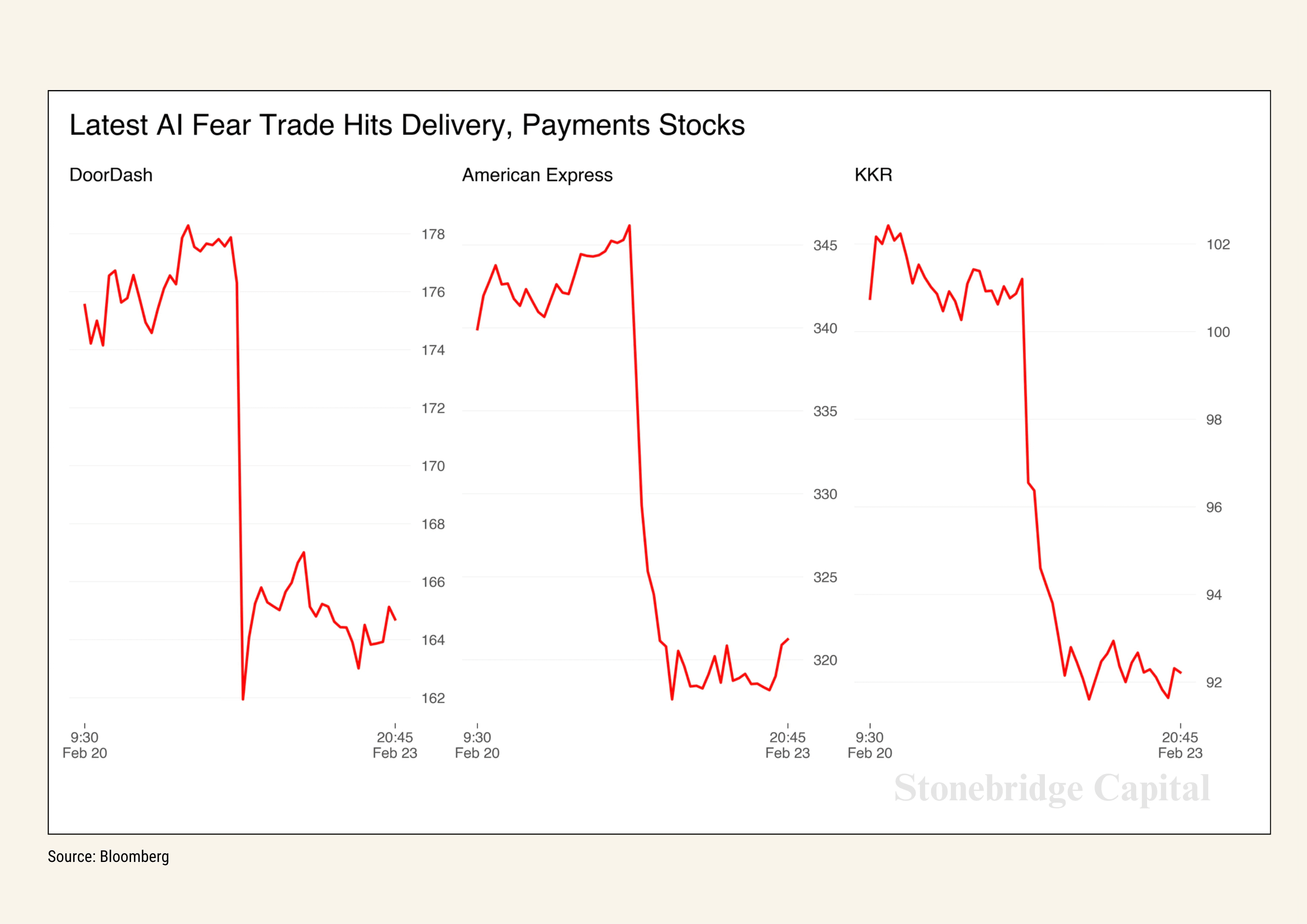

Just as software stocks were starting to stabilize, Claude Code Security arrived. In February 20, Crowdstrike was among the biggest decliners, falling 8%, while Cloudflare slumped 8.1%. Zscaler dropped 5.5%, SailPoint shed 9.4%, and Okta declined 9.2%. The Global X Cybersecurity ETF fell 4.9% and closed at its lowest since November 2023.

Investors feared that AI-powered tools like Claude Code Security could partially replace established cybersecurity products and services. The concern focuses on the possibility that automated vulnerability detection through AI could reduce demand for traditional scanning tools and exert price pressure on providers.

The selloff is the second that Anthropic has set off in the enterprise software ecosystem since the start of the month.

What’s Actually Happening Here

The honest take is that the panic is partly rational and partly overdone. In a research note, Wedbush Securities said that while AI is a headwind for software providers, the selloff reflected an “Armageddon scenario for the sector that is far from reality.” Enterprises won’t completely overhaul tens of billions of dollars of prior software infrastructure investments overnight.

At the same time, as James St. Aubin, chief investment officer at Ocean Park Asset Management, put it: “The selloff is a manifestation of an awakening to the disruptive power of AI. The seemingly wide moats of these companies feel a lot more narrow today as competition from AI-created products intensifies. Perhaps this is an overreaction, but the threat is real and valuations must account for that.”

Both of these things can be true simultaneously. Short-term, the selloff is likely exaggerated. Structurally, the shift toward AI agents eating into the “application layer” is real and accelerating.

2026 Outlook and the Investor Playbook

The Macro Setup

The sector has lost around $2 trillion of market capitalization from its peak as investors grow concerned about AI’s potential to disrupt those businesses. That’s a lot of fear priced in. The question is whether the fear is ahead of the reality, behind it, or roughly calibrated.

The answer probably varies by category. Legal databases and research aggregators that charge premium subscription fees for content Claude can now synthesize are structurally exposed. Horizontal SaaS platforms with deep workflow integrations, large enterprise data moats, and aggressive AI roadmaps are different from pure-play data vendors.

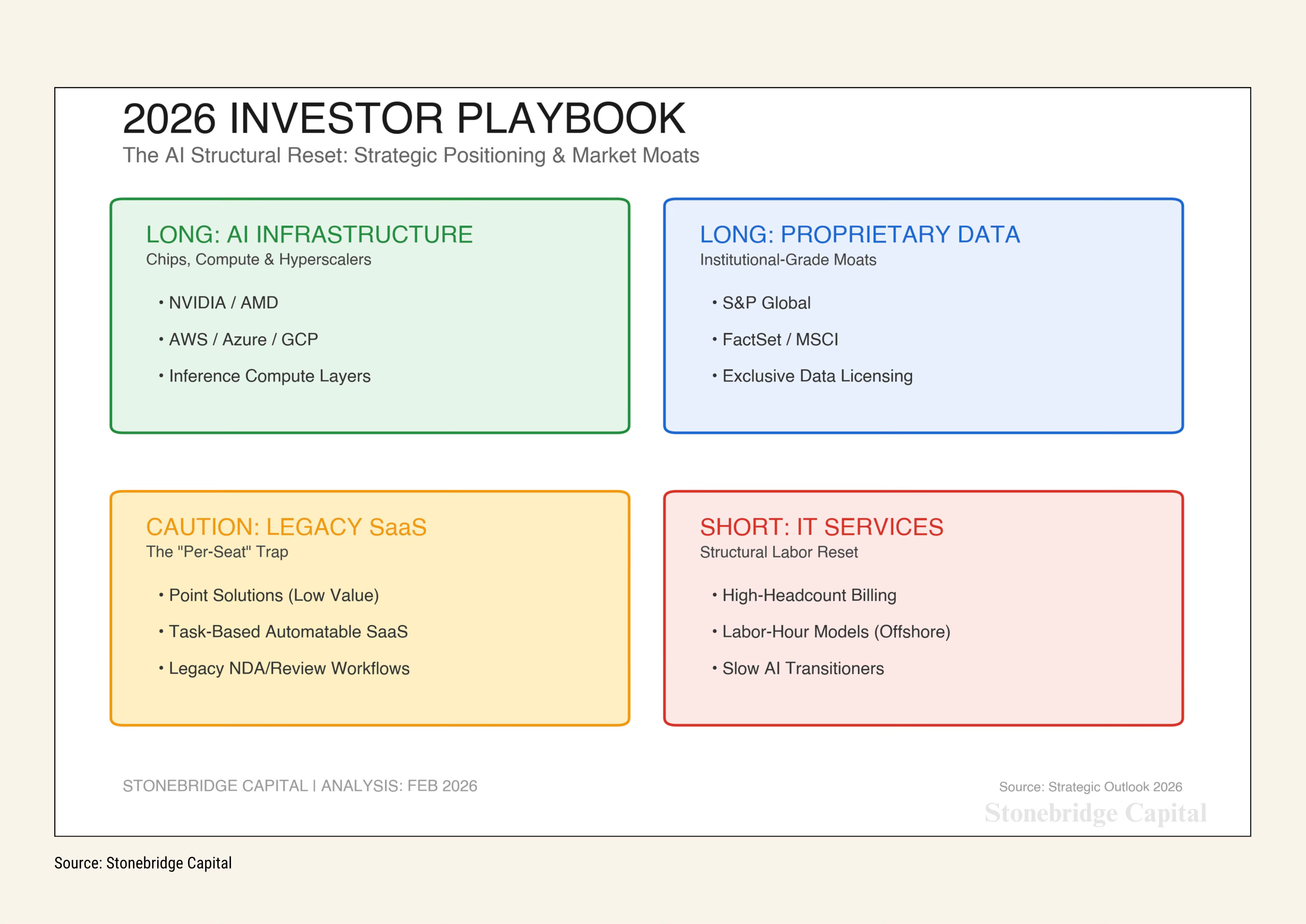

Winners

The infrastructure layer keeps printing. Nvidia, AMD, and the cloud hyperscalers (AWS, Google Cloud, Azure) are direct beneficiaries of every model release — every Opus 4.6 inference run goes through their chips and data centers. That relationship doesn’t change regardless of which AI lab is winning model benchmarks.

Data providers with proprietary, hard-to-replicate datasets — S&P Global, FactSet, MSCI in their core business lines — are more nuanced. Claude can synthesize public information. It can’t replicate exclusive data licensing agreements or institutional-grade alternative data sets. Companies that understand this distinction and position accordingly will hold their ground.

Software companies that are embedding Claude natively rather than competing with it are a separate category. The enterprises that white-label Claude capabilities into their existing products, or use Claude Code to ship product faster, are augmenting rather than being displaced.

The Losers (or the Value Traps)

Legacy SaaS with per-seat pricing models built on low-value, automatable tasks is where the structural risk is highest. If a Claude Cowork plugin can review an NDA or build a financial model, the incremental per-seat fee charged by a point solution becomes a harder sell.

High-headcount IT services firms — particularly those in India running billing models tied to labor hours — face a structural reset. AI-driven automation raises uncomfortable questions about utilisation rates, pricing models, and long-term demand for large delivery teams. The Nifty IT index has felt this already.

Pure-play cybersecurity vendors that are slow to integrate AI-native capabilities into their stack are exposed to both the Claude effect and the broader shift toward proactive, automated security rather than reactive monitoring.

Your Moves Right Now

Use the tools yourself before making portfolio calls. The free tier of claude.ai with Sonnet 4.6 as the default model gives you immediate access to test the finance and research capabilities firsthand. Pro and Max plans unlock the full agentic stack including Claude Code. The best research you can do before adjusting your software holdings is to run the prompts described earlier and judge the output quality directly.

For portfolio positioning, the framework is straightforward: long AI infrastructure (chips, compute, cloud), selectively long on companies actively embedding AI to accelerate product and margin, and cautious on legacy SaaS categories most exposed to direct substitution. Specific names need individual analysis of their AI roadmaps and data moat depth, which is worth doing before the market fully reprices every category.

Watch three metrics in the months ahead: Anthropic’s revenue run-rate (currently at $14B and growing fast), the pace of enterprise win announcements, and whether the Cowork and Claude Code adoption numbers keep compounding. Business subscriptions to Claude Code have quadrupled since the start of 2026. The number of customers spending over $100,000 annually has grown 7x in the past year. Two years ago, a dozen customers spent over $1 million with Anthropic on an annualized basis. Today that number exceeds 500.

That trajectory is the underlying signal that matters more than any single stock selloff.

The Bottom Line

Claude isn’t coming for jobs as an abstraction — it’s coming for specific, well-compensated workflows in finance, law, software development, and cybersecurity. The investors who treat it as a co-pilot for their own research today will have a genuine information edge. The companies whose entire product roadmap amounts to “we’ll add some AI features soon” are the ones who should be worried.

The selloff has created pockets of genuine value in quality software businesses with real AI integration — and pockets of still-overpriced names that markets haven’t fully repriced yet. The Claude Effect is ongoing. The February turbulence was a preview, not a conclusion.

Try the research prompts above and reply with the most interesting output you get. I’ll feature the sharpest Claude-generated trade ideas in the next edition. Next week: my full 2026 AI stock basket and a Claude-powered valuation template you can use yourself.

This article is for informational and educational purposes only and does not constitute financial advice. All investment decisions involve risk.