It's All About Power Now

Inside the AI infrastructure arms race that's reshaping the power grid

For the last three years, the “AI Trade” was a simple equation: Buy the chips. If you owned Nvidia, you won. The semiconductor giant’s stock became a proxy for the entire artificial intelligence revolution, and for good reason—without GPUs, there is no AI. But as we settle into 2026, the easy money in silicon has been made, and the market’s focus has aggressively rotated. The bottleneck is no longer just about acquiring H100s or Blackwells—it’s about plugging them in.

The “Great Rotation” from chips to concrete is now fully underway. We are witnessing the largest industrial capital deployment in history, a transition from digital speculation to physical industrialization. The latest earnings season confirms that the hyperscalers are not blinking; they are doubling down. But they are running headlong into a physical wall: the power grid.

What’s becoming clear is that the AI revolution won’t be won in software labs or semiconductor fabs—it will be won in electrical substations, cooling towers, and transmission line corridors. The companies that can secure gigawatts will control the future of AI. Those that can’t will find themselves with the most sophisticated chips in the world and nowhere to run them.

Here is the updated state of play for the AI Infrastructure trade in 2026.

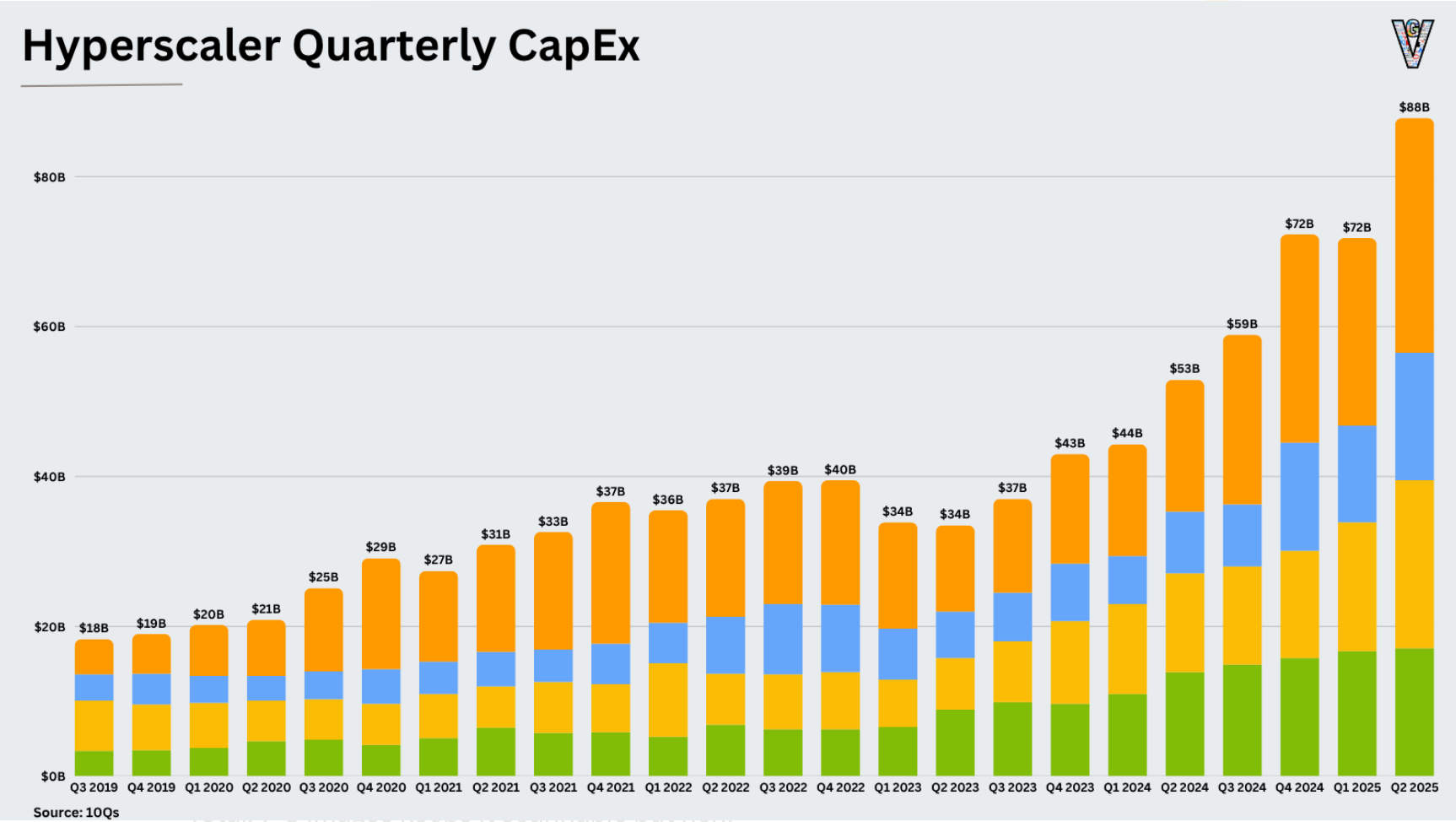

1. The $700 Billion Capex Floor

If there was any doubt that the AI spending cycle might peak in 2025, the last two weeks of earnings calls shattered it. The combined 2026 capital expenditure guidance from the “Big Four” (Amazon, Microsoft, Alphabet, Meta) has now breached the $650–$700 billion mark—a figure that exceeds the GDP of many mid-sized nations and represents more capital deployment than the entire U.S. construction industry generated in 2024.

Amazon’s $200 billion capex plan for 2026 represents a 53% jump from 2025 levels. While the market initially balked—sending shares down approximately 9% on free cash flow concerns—the signal is unambiguous: AWS is constrained by capacity, not demand. CEO Andy Jassy made this explicit on the earnings call, stating that the company is turning away customers due to compute shortages. In Amazon’s calculus, the risk of not spending is greater than the risk of over-building.

The company’s investor letter was remarkably candid about the physics of the problem. AWS currently operates in 33 geographic regions, but the bottleneck isn’t regional footprint—it’s raw power availability. Amazon admitted that several planned 2025 data center expansions in Northern Virginia were delayed by 18-24 months purely due to grid interconnection timelines. The $200 billion isn’t just about servers and chips; it’s increasingly about transformers, switchgear, and the unsexy infrastructure required to deliver electrons at industrial scale.

Google & Microsoft Follow Suit: Alphabet (GOOGL) guided for $175–$185 billion in 2026 spend, citing “tight supply environments” for AI compute. What’s notable is the composition shift. CFO Ruth Porat disclosed that roughly 40% of the 2026 budget is now allocated to “enabling infrastructure”—a euphemism for power generation, cooling systems, and land acquisition. This is up from just 25% in 2024.

Microsoft (MSFT) is pacing toward $145 billion, and CEO Satya Nadella’s language on the earnings call was telling. He repeatedly used the term “energy partnerships” rather than “data center builds,” signaling that Microsoft views power procurement as the strategic moat. The company has signed over a dozen power purchase agreements in the past six months alone, ranging from wind farms in Iowa to geothermal projects in Nevada.

Meta (META) has tightened its range to $115–$135 billion, with Zuckerberg explicitly pivoting spend toward power and data center shells rather than just servers. The subtext: Meta is pre-positioning for a 2027-2028 AI training push, but the company has learned from the hyperscalers’ 2024-2025 pain that you can’t just show up and demand 500 megawatts. You need to own the electrons.

The Takeaway: The “Capex Wall” is higher than even the bulls predicted. Goldman Sachs’ late-2025 estimate of a $1.4 trillion three-year spend now looks conservative. Morgan Stanley’s infrastructure team published a note last week revising their estimates upward to $1.6–$1.8 trillion through 2028. For the infrastructure supply chain, this is a multi-year backlog guarantee. The spending isn’t discretionary anymore—it’s defensive.

2. The Power Crunch: “The Coming Age of Electricity”

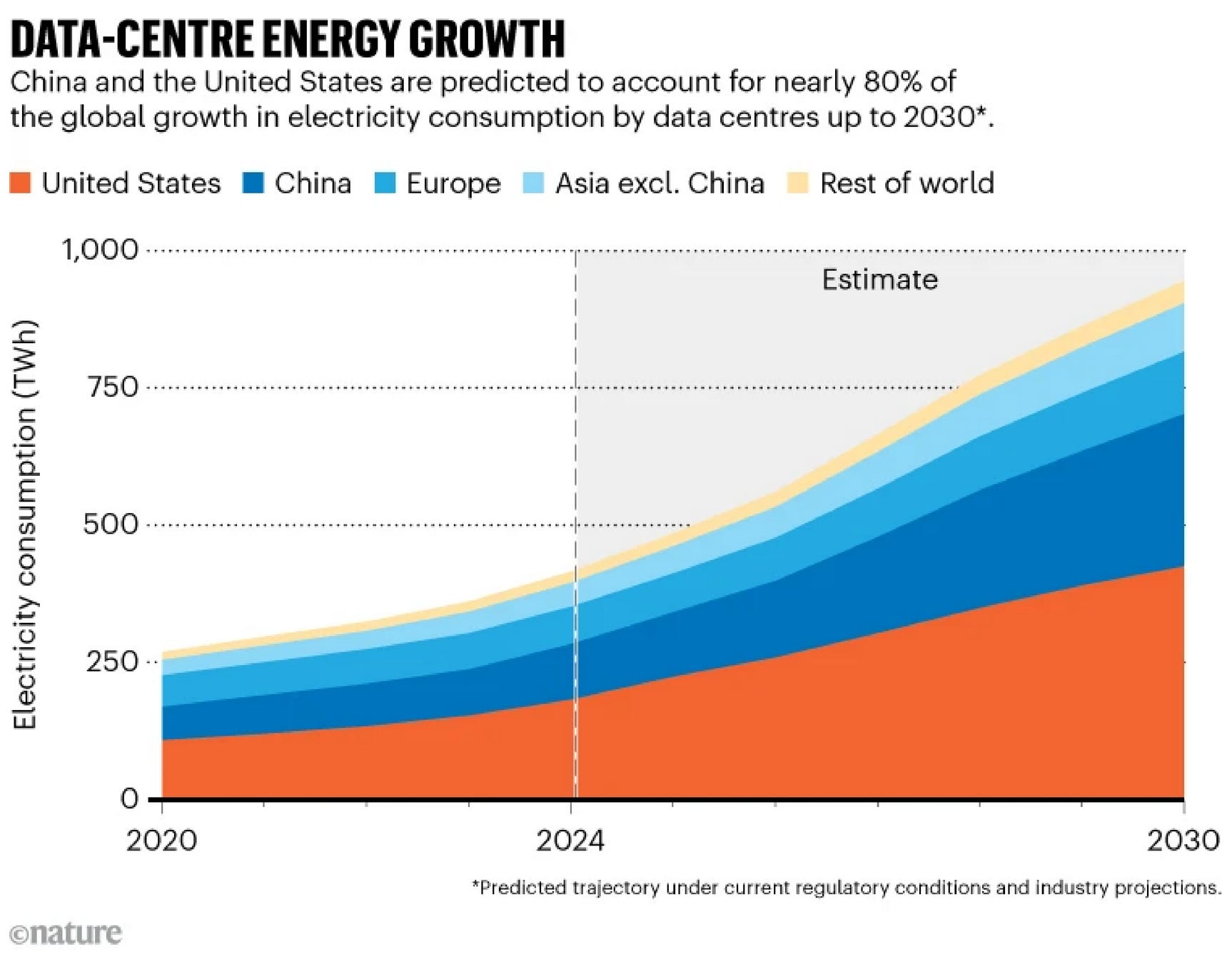

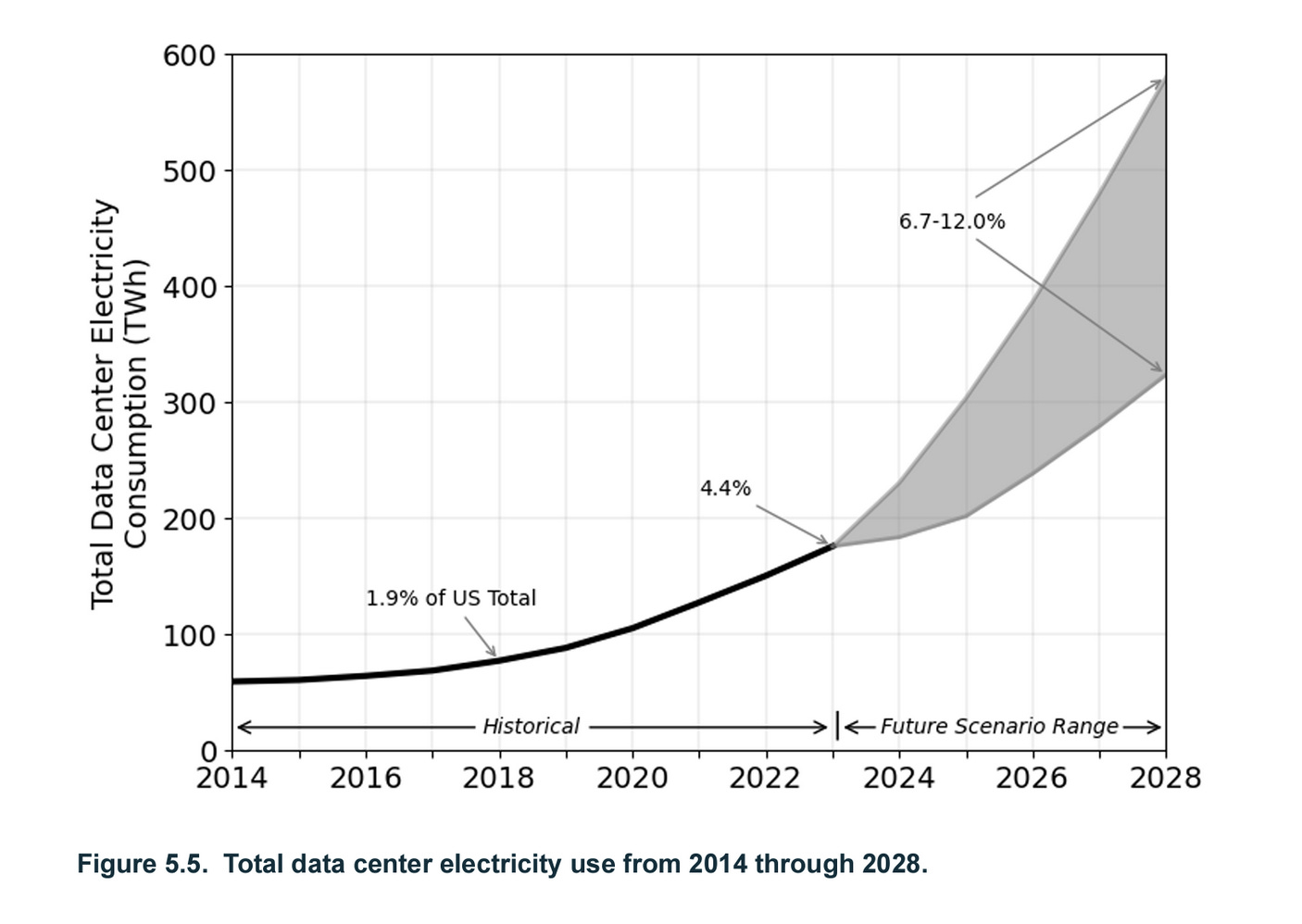

The physical constraints of the grid are no longer a theoretical risk; they are the primary governor on AI growth. The International Energy Agency (IEA) released its updated Electricity 2026 report last week, forecasting that U.S. data center electricity consumption will exceed 250 TWh this year—on its way to tripling by 2030. To put that in perspective, 250 TWh is roughly equivalent to the entire annual electricity consumption of Australia.

The IEA explicitly notes that while overall U.S. demand is growing at a modest 2% annually, regional grids in Northern Virginia (PJM), Texas (ERCOT), and Ireland are flashing red. The problem isn’t national capacity—it’s local distribution. The grid wasn’t designed for point-load concentrations of 500+ megawatts in a single location. Utilities are being asked to deliver industrial-scale power to what were, five years ago, relatively sleepy suburban corridors.

Gridlock in PJM: The PJM Interconnection queue remains the choke point. Despite reform efforts in 2025, the backlog for new generation connection requests still hovers above 2,000 GW. To be clear, not all of those projects will be built, but the sheer volume indicates how overwhelmed the system has become. The wait time for a new hyperscale facility to get “energized” in prime markets like Loudoun County, Virginia—the epicenter of global data center activity—has stretched to 4–6 years.

This isn’t just bureaucratic red tape. The physical grid in Northern Virginia is operating near capacity during peak demand periods. Adding another gigawatt of data center load requires not just new substations, but often new transmission lines from generation sources that may be 100+ miles away. PJM has been transparent about this: the transmission infrastructure to support the planned data center buildout simply doesn’t exist yet, and building it takes time.

The Shift: This is forcing hyperscalers to abandon prime markets and get creative. Microsoft’s recent land acquisitions in Southern Europe—particularly in Spain and Portugal—are direct responses to PJM’s saturation. The company is betting on Iberian wind and solar resources, combined with more permissive local regulations. Amazon’s expansion into the chaotic energy markets of the Midwest, including a controversial project in rural Ohio, reflects similar logic: go where the power is available, even if the latency isn’t optimal.

We’re also seeing a geographic dispersion that would have been unthinkable two years ago. Data centers are now being proposed in Montana, Wyoming, and the Dakotas—states with surplus renewable energy but limited tech infrastructure. The era of “cluster everything in Ashburn” is over.

3. Power Generation: The Nuclear Renaissance (and its Limits)

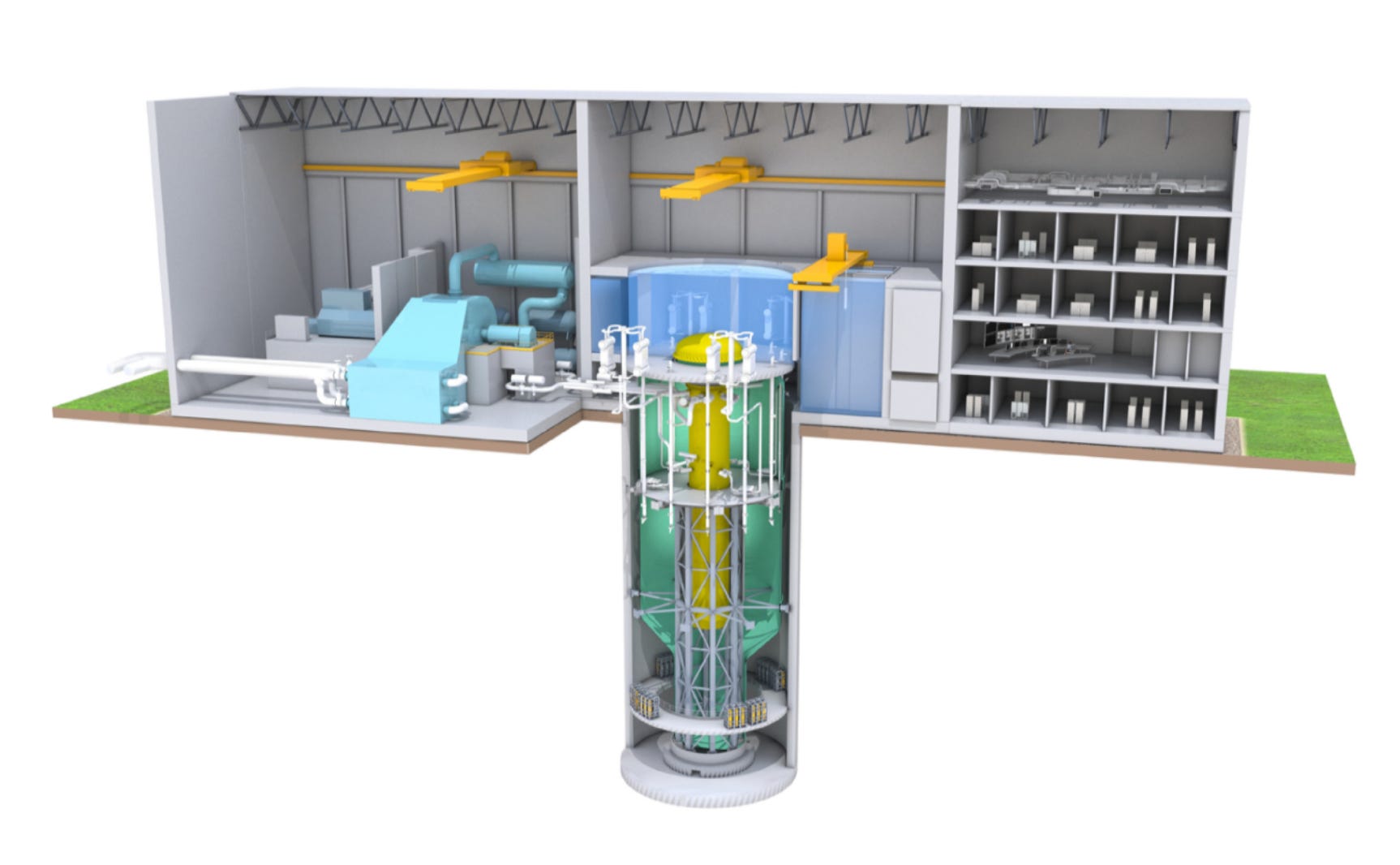

The “Nuclear Renaissance” is the most seductive narrative in the sector, but 2026 has brought a dose of reality. The divergence between behind-the-meter dreams and grid-level reality is stark. Nuclear power offers what AI training clusters desperately need: always-on baseload power with zero carbon emissions. But the path from concept to kilowatt-hour is littered with regulatory hurdles, community opposition, and physics.

The Bull Case (Constellation/Microsoft): The deal of the decade remains Constellation Energy’s (CEG) restart of Three Mile Island Unit 1, now rebranded as the “Crane Clean Energy Center.” Updates from Constellation last month confirm the project is ahead of schedule for a 2027 energization, with Microsoft buying every electron for 20 years under a power purchase agreement worth an estimated $10+ billion.

This is the blueprint every hyperscaler wants to replicate: dedicated, reliable, carbon-free power with no grid dependency. Microsoft doesn’t just get electricity; it gets certainty. In a world where grid access can delay a project by half a decade, that certainty is worth paying a premium. The deal also locks in pricing, insulating Microsoft from the wild swings in regional electricity markets that have plagued data center operators in Texas and other deregulated grids.

Constellation’s stock has more than doubled since the deal was announced in late 2024, and the company is now actively shopping its other nuclear assets to hyperscalers. The message is clear: nuclear baseload is the new “sovereign territory” for AI infrastructure. Whoever controls the atoms controls the future.

The Bear Case (Talen/Amazon): However, the regulatory moat is real, and FERC is not playing along. Following FERC’s rejection of the expanded Amazon-Talen Energy (TLN) interconnection agreement in late 2024—a deal that would have allowed Amazon to co-locate a data center directly next to Talen’s Susquehanna nuclear plant in Pennsylvania—the agency doubled down in its April 2025 guidelines.

FERC has signaled it will not allow hyperscalers to “cut the line” and siphon nuclear baseload power at the expense of residential and commercial reliability. The commission’s concern is straightforward: if Amazon gets to plug directly into Susquehanna and take 500+ megawatts off the grid, who compensates the Pennsylvania ratepayers who funded that plant’s construction? And what happens when a winter storm hits and residential demand spikes, but the electrons are contractually locked up in a data center?

This effectively kills the easy “co-location” trade for now, forcing hyperscalers to fund new generation rather than just plugging into existing plants. The economics are far less attractive when you’re paying for reactor restarts or new small modular reactors (SMRs) that won’t be online until 2030 or later.

There’s also the SMR wildcard. Companies like TerraPower, X-energy, and NuScale have collectively raised billions in venture capital and government funding, promising factory-built reactors that can be deployed in 3-5 years instead of the decade-plus timelines of traditional nuclear. Google and Amazon have both signed letters of intent with SMR developers. But as of February 2026, not a single commercial SMR is operating in the United States. The technology is promising, but it’s not solving the 2026-2028 power crunch

.

4. The Builders: Backlogs Don’t Lie

While the utilities fight over regulation and the hyperscalers negotiate power deals, the companies actually building the grid are printing money. The “picks and shovels” trade has moved from the GPU makers to the electrical contractors, cooling specialists, and transformer manufacturers. These are decidedly unsexy businesses, but their order books tell the real story of where the capital is flowing.

Quanta Services (PWR): The electrical infrastructure giant reported a record backlog of $39.2 billion in its most recent earnings, up 28% year-over-year. To put that in context, Quanta’s backlog is now larger than the company’s total revenue over the past two years combined. They are the only player with the scale to handle the transmission line buildout required to uncork the grid.

The company’s CEO made an interesting comment on the earnings call: “We’re not capacity-constrained by capital or demand—we’re constrained by skilled labor.” Quanta is hiring electrical lineworkers as fast as they can train them, and they’re still turning down projects. The subtext: this isn’t a one-year sugar rush. The transmission infrastructure required to support the AI buildout will take the better part of a decade to complete.

Quanta’s largest customers are now the hyperscalers themselves, not the utilities. Amazon, Microsoft, and Google are directly funding transmission projects to connect their data centers to generation sources, rather than waiting for utilities to act. This is a fundamental shift in how infrastructure gets built in America—private capital is now stepping in to build what was historically public utility infrastructure.

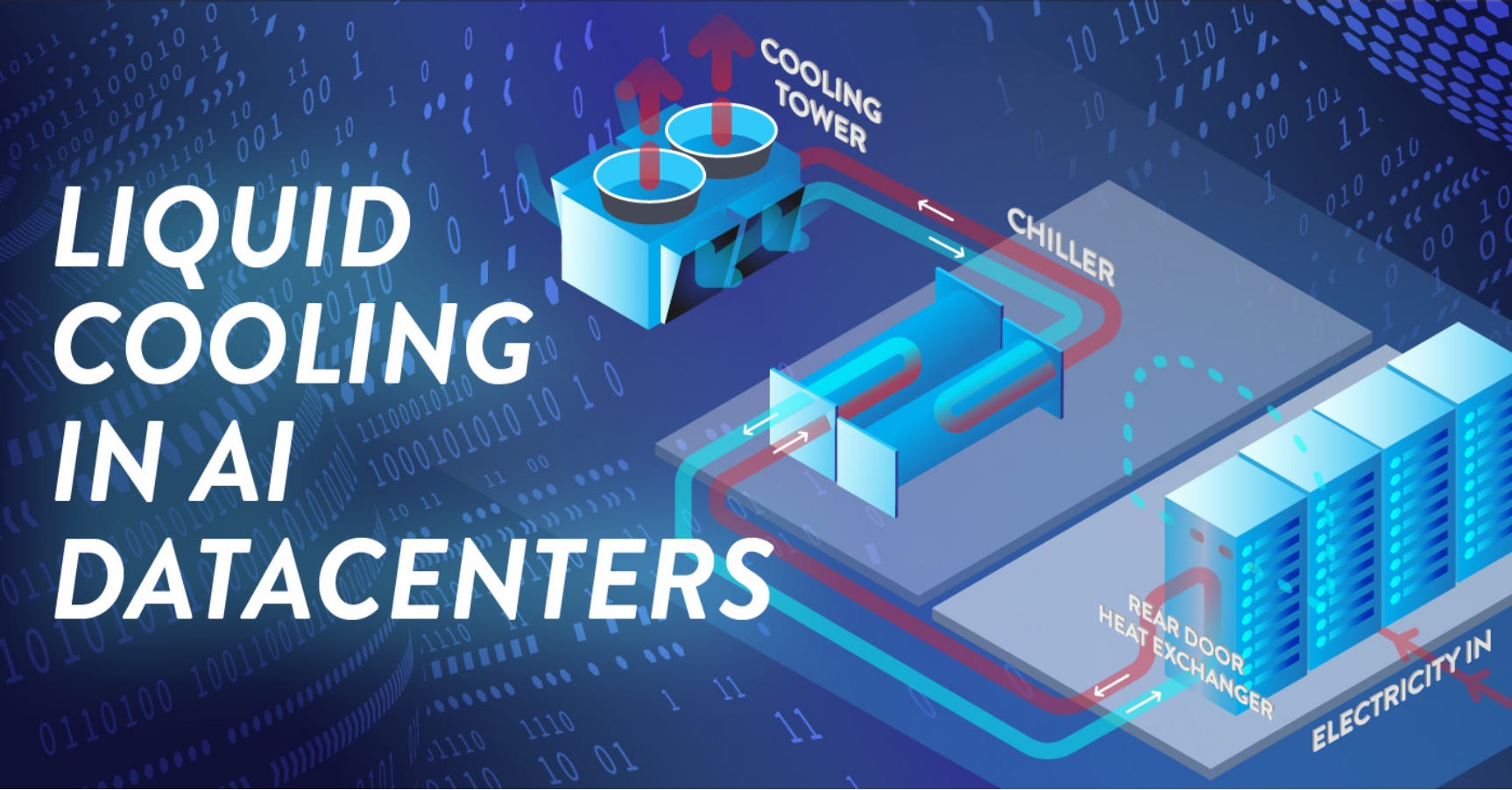

Vertiv (VRT): The shift to liquid cooling is absolute, and Vertiv has emerged as the dominant player. With Nvidia’s Blackwell and upcoming Rubin chips demanding rack densities of 100kW or more, air cooling is obsolete for frontier AI training clusters. You simply can’t move enough heat with air at those power densities. Liquid cooling—either direct-to-chip or full immersion—is the only viable solution.

Vertiv reported a 60% year-over-year increase in organic orders in Q3 2025, and the company’s backlog for liquid cooling systems now extends into late 2027. They’ve effectively cornered the market on high-density thermal management, and their customers have no choice but to wait in line. The company is building new manufacturing capacity as fast as possible, but even that takes time.

What’s notable is the margin expansion. Vertiv’s liquid cooling systems command 2-3x the gross margin of traditional air cooling, and customers aren’t negotiating on price because they have no alternatives. The company’s stock has been one of the best-performing names in the industrial sector over the past 18 months, and analysts see no reason for that to change.

The Transformer Bottleneck: One underappreciated constraint is transformers—the massive electrical components that step down high-voltage transmission power to usable levels. The global supply chain for large power transformers was already tight before the AI boom, and lead times have now stretched to 24-36 months. These aren’t off-the-shelf items; they’re custom-engineered pieces of equipment that can weigh over 400 tons and cost millions of dollars each.

A single hyperscale data center might require a dozen or more transformers, and if even one is delayed, the entire facility sits idle. Utilities and hyperscalers are now ordering transformers two to three years in advance of anticipated need, just to secure capacity. This has created a de facto cartel among the handful of manufacturers that can produce these units at scale, with companies like ABB, Siemens, and Hyundai Heavy Industries holding extraordinary pricing power.

5. Risks: The “Monetization Gap”

Despite the bullish infrastructure setup, the risks in 2026 are distinct from 2024, and they’re starting to show up in stock prices and analyst reports. The enthusiasm that greeted every AI announcement in 2024 has given way to a more hard-nosed focus on returns.

Margin Compression: Amazon’s stock drop last week was a warning shot that can’t be ignored. The market gave hyperscalers a free pass in 2024 and 2025 to spend whatever it took to win the AI race. But investors are now starting to punish companies that burn cash on capex without immediate AI revenue realization. Amazon’s free cash flow guide for 2026 was deeply negative, and the CFO’s explanation—that AWS growth justifies the spend—wasn’t enough to calm jittery investors.

The “Monetization Gap”—the difference between capex spend and incremental AI revenue—is widening, not narrowing. Microsoft is the only hyperscaler that can credibly point to AI revenue (via Copilot and Azure AI services) that’s growing faster than AI capex. Google’s AI revenue is still mostly ads-adjacent, Meta is spending $100+ billion with no clear near-term revenue path, and Amazon won’t break out AI revenue separately.

If the Monetization Gap continues to widen through Q2 and Q3 2026, we could see a significant pullback in infrastructure spending plans. The bulls argue that AI revenue will inflect in late 2026 or 2027 as enterprise adoption scales, but the bears are losing patience. A few more quarters of “spend now, monetize later” and we could see a 2000-style reckoning where the market stops funding growth at any price.

Community Pushback: The “Not In My Backyard” (NIMBY) movement has gone global, and it’s becoming a legitimate operational risk. Virginia’s recent moratorium discussions on new data center approvals in Prince William County sent shockwaves through the industry. Loudoun County, the data center capital of the world, is now facing organized opposition from residents concerned about water usage, noise pollution, and the industrialization of what were once rural communities.

These aren’t fringe protestors—they’re county supervisors, school boards, and chambers of commerce. The backlash is spreading to new hubs like Arizona, Georgia, and even Texas, where you’d expect a more business-friendly environment. Water usage is a particularly acute issue. A single large data center can consume millions of gallons of water per day for cooling, and in drought-prone regions, that’s putting data centers in direct competition with agriculture and residential use.

Dublin, Ireland—a major European data center hub has imposed strict power caps that effectively prevent new large-scale facilities from being built. The city’s grid can’t handle additional load, and residents have made it clear they don’t want their electricity bills subsidizing hyperscaler AI ambitions. Similar dynamics are playing out in Singapore, Amsterdam, and other dense urban markets.

The litigation risk is also escalating. Environmental groups are filing lawsuits to block projects on water usage, greenhouse gas emissions (even for “carbon-neutral” facilities), and habitat destruction. These lawsuits can stall projects for years, even if they ultimately lose in court. The permitting and community approval process, once a 6-12 month formality, is now stretching to 2-3 years in contested jurisdictions.

6. The Geopolitical Wildcard

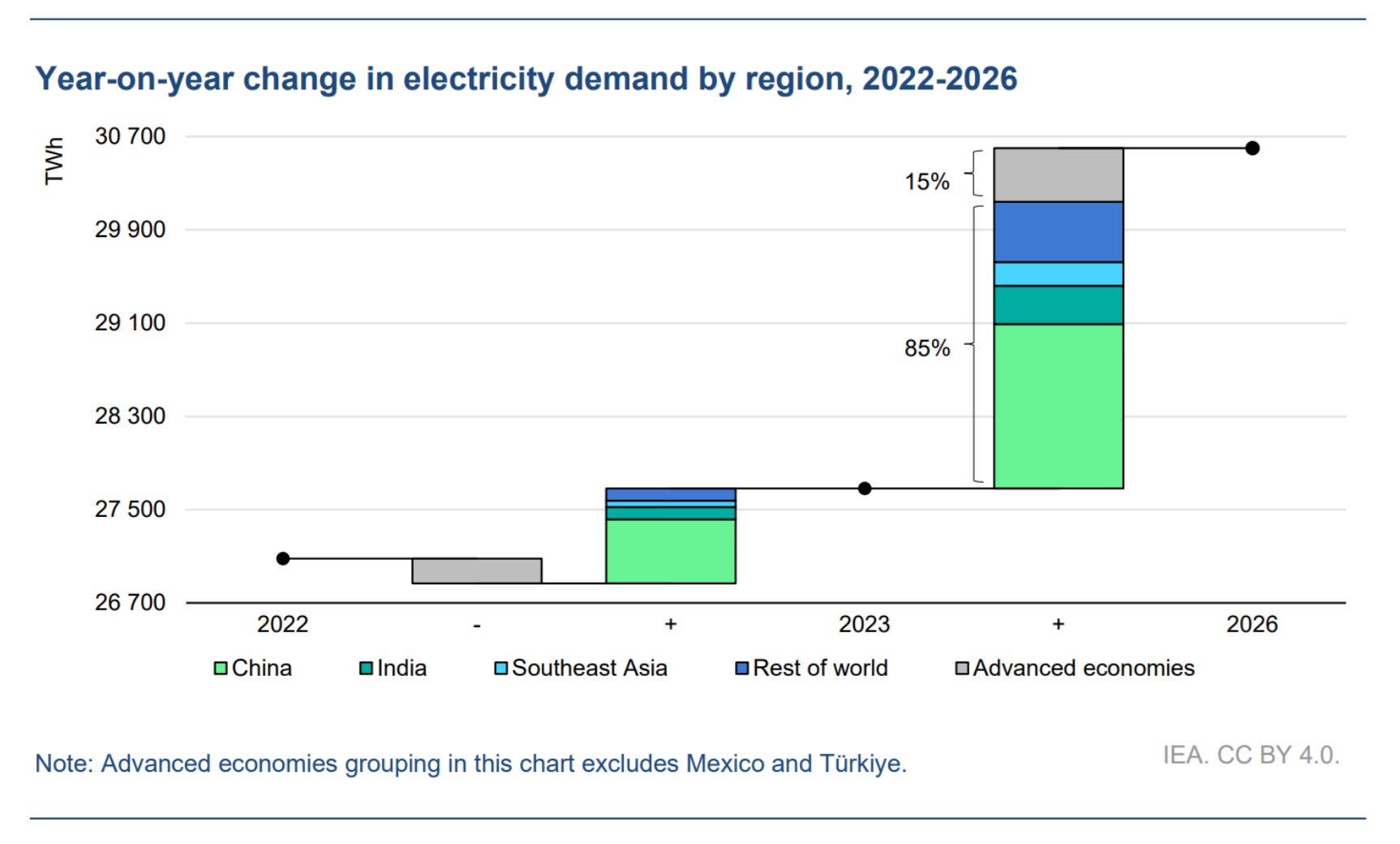

One underappreciated dimension of the infrastructure race is geopolitics. The U.S. still holds a commanding lead in AI infrastructure, but China is making massive investments, and the European Union is trying to avoid becoming a digital colony.

China’s State-Led Push: While Western hyperscalers wrestle with FERC regulations and NIMBY opposition, China’s state-owned enterprises are building data centers at a pace that would be impossible in a market economy. The government has designated AI infrastructure as a strategic priority, and provincial governments are competing to offer the most attractive incentives. China doesn’t have a PJM queue problem—it has a centrally planned grid that can prioritize AI load over other uses.

The wild card is whether China’s domestic AI models can compete with Western frontier models. If they can, China’s infrastructure advantage could translate into AI dominance. If they can’t, all that infrastructure spend is wasted capital. We’ll have a clearer answer by the end of 2026 as China’s national AI champions release their next-generation models.

Europe’s Dilemma: Europe is caught in the middle. It has some of the world’s strictest data privacy and environmental regulations, making it difficult to build hyperscale infrastructure. But European governments are increasingly nervous about being entirely dependent on U.S. and Chinese AI systems. The EU’s proposed “Sovereign AI” initiative would fund domestic data centers and AI development, but the budget is a fraction of what the hyperscalers are spending.

The more likely outcome is that Europe becomes a customer of U.S. AI systems, not a producer. That has strategic implications that EU policymakers are only beginning to grapple with.

Investment Implications

The “easy” phase of the AI trade is over. The 2026 winner will not be the company with the best chatbot, but the company with the most secured power. The market is slowly coming to terms with this reality, and the capital rotation is accelerating.

Overweight: Grid infrastructure plays like Quanta Services and Eaton are still in the early innings of a multi-year buildout cycle. These companies have visible, contracted revenue stretching years into the future, and they’re trading at reasonable multiples relative to growth. Unregulated power producers with existing capacity—Constellation, Vistra, and to a lesser extent NRG—are the scarcest assets in the market. Nuclear baseload is digital gold, and the hyperscalers will pay up for it.

Cooling and thermal management is another area with strong tailwinds. Vertiv is the obvious name, but there’s room for smaller players like Schneider Electric and Johnson Controls to take share in specific niches.

Watch: The “Monetization Gap” is the single biggest risk to the entire thesis. If Microsoft or Google hint at capex cuts during their July earnings calls, the entire industrial trade will re-rate lower. The market is currently willing to look through near-term profitability concerns, but that patience isn’t infinite.

Also watch the regulatory environment. FERC’s stance on nuclear co-location could shift with a new administration or new commissioners, and that would meaningfully change the economics of the nuclear trade. Similarly, if more jurisdictions follow Dublin’s lead and cap data center power consumption, the geographic options for hyperscalers narrow considerably.

For now, the guidance is clear: The checkbooks are open, the concrete is pouring, and the grid is the only limit. The companies that solve the power problem will own the AI future. Those that don’t will be left with expensive chips and nowhere to run them.

The 2026 AI Infrastructure Playbook is simple: Follow the electrons.

Disclaimer: This article is intended for informational purposes only and should not be construed as personalized financial advice. Stonebridge Capital may hold positions in securities mentioned in this analysis. All investing involves risk, including the potential loss of principal.